As we enter the second half of 2023, the environment couldn’t be more different from the same point one year ago. In the middle of 2022, stock prices were falling rapidly, inflation was peaking, the Fed was in the early stages of an aggressive rate-hiking campaign, volatility was elevated, and bonds sustained one of their worst selloffs in modern history.

Fast forward to today and the investing picture looks pretty different. Equities have had a strong start to the year, especially technology stocks. Bond yields (and prices) are pretty much in line with where they started the year, though they have been fairly volatile along the way. The Fed has eased up on rate hikes, having increased only three times in 2023, and each hike was only 25 basis points. Inflation has fallen to below 5% by almost every measure, well below the highs it hit in 2022.

The one thing that remains the same is uncertainty around if or when the U.S. economy will enter a recession, as well as the prognosis for various asset class returns if that happens. The timing and severity of a recession depends a lot on how aggressive central banks continue to be, which will in turn depend on how quickly inflation falls from here. There are a few items worth watching over the coming months as they will help determine where equity and bonds markets go next.

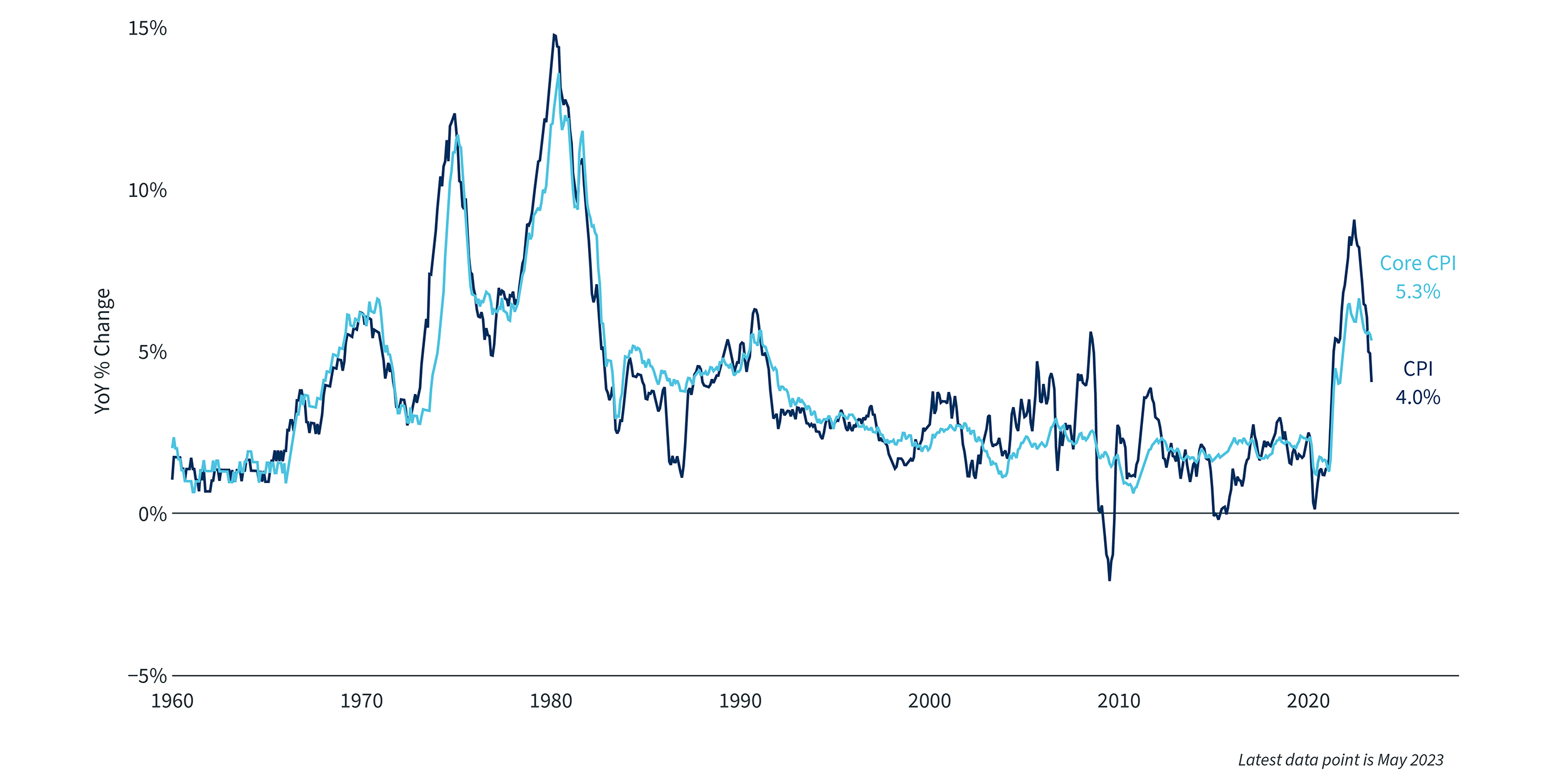

Inflation is falling, but slowly

Inflation has been one of the biggest news stories over the past 18 months. After decades of fairly benign inflation in the U.S. – with almost as many potentially deflationary periods as inflationary – inflation unexpectedly took off around the world in early 2022 and is generally still well above central bank targets.

Inflation initially fell quite quickly from its highs in the middle of last year, but recently the pace of decline has slowed. Core inflation, which excludes food and energy, has actually flattened out for the past 6-8 months, remaining stubbornly in the 4.5% to 5% range throughout 2023. A lot of prices, especially in the services industry, are proving sticky, which may require even higher central bank rates and higher unemployment levels to bring down. As housing prices stabilize or even fall slightly, the core rate of inflation may start to fall as well, but it may take a slowing economy to really get inflation close to the 2% target the Fed and other central banks have set as their goal.

Consumer Price Index1

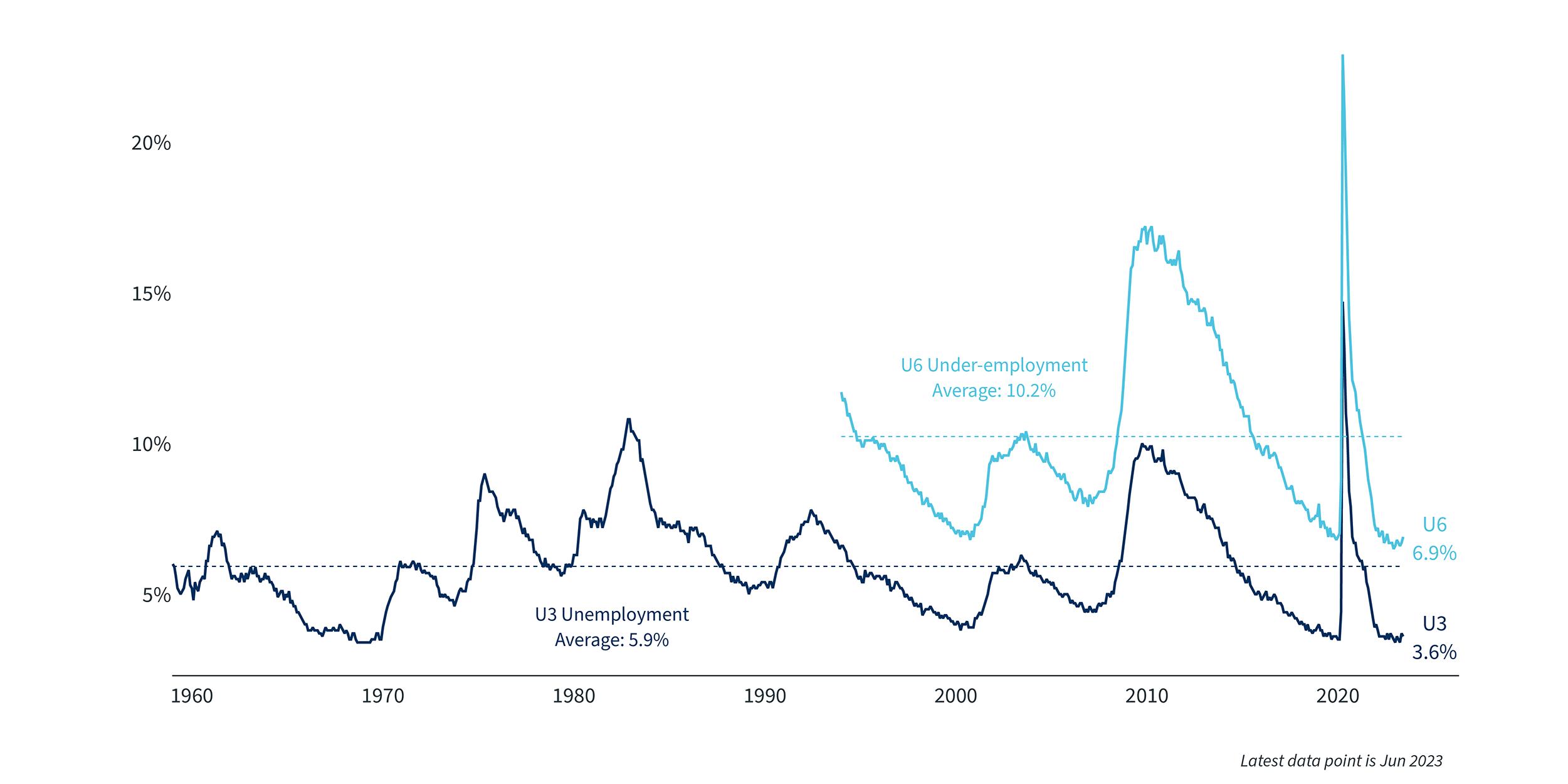

Labor markets and GDP continue to defy predictions of a slowdown

Despite the rapid rise in interest rates last year, the economy has proven remarkably strong. This is mainly due to the strength in the labor market and the related stability in consumer spending. The U.S. unemployment rate has hovered between 3.4% and 3.7% for well over a year, a remarkable run of strength. Labor force participation has been rising, which is a good sign, though it is still below the pre-pandemic average, and wages have been growing steadily but not excessively.

As consumers feel confident about their job prospects and achieve wage growth in the 4-5% range, they have in turn used their increased earnings and their excess savings from pandemic-related stimulus checks to buy goods and services, particularly those related to travel and entertainment. While most of the excess savings has now been used up, solid wage growth continues to propel consumer spending.

As a result of the strong labor market, first-quarter GDP was a solid 2%, well above expectations from the beginning of the year and barely below the fourth quarter of 2022. The early signs for second-quarter GDP are also looking positive, as the highly anticipated Fed-induced recession remains perennially six months off.

Unemployment Rates2

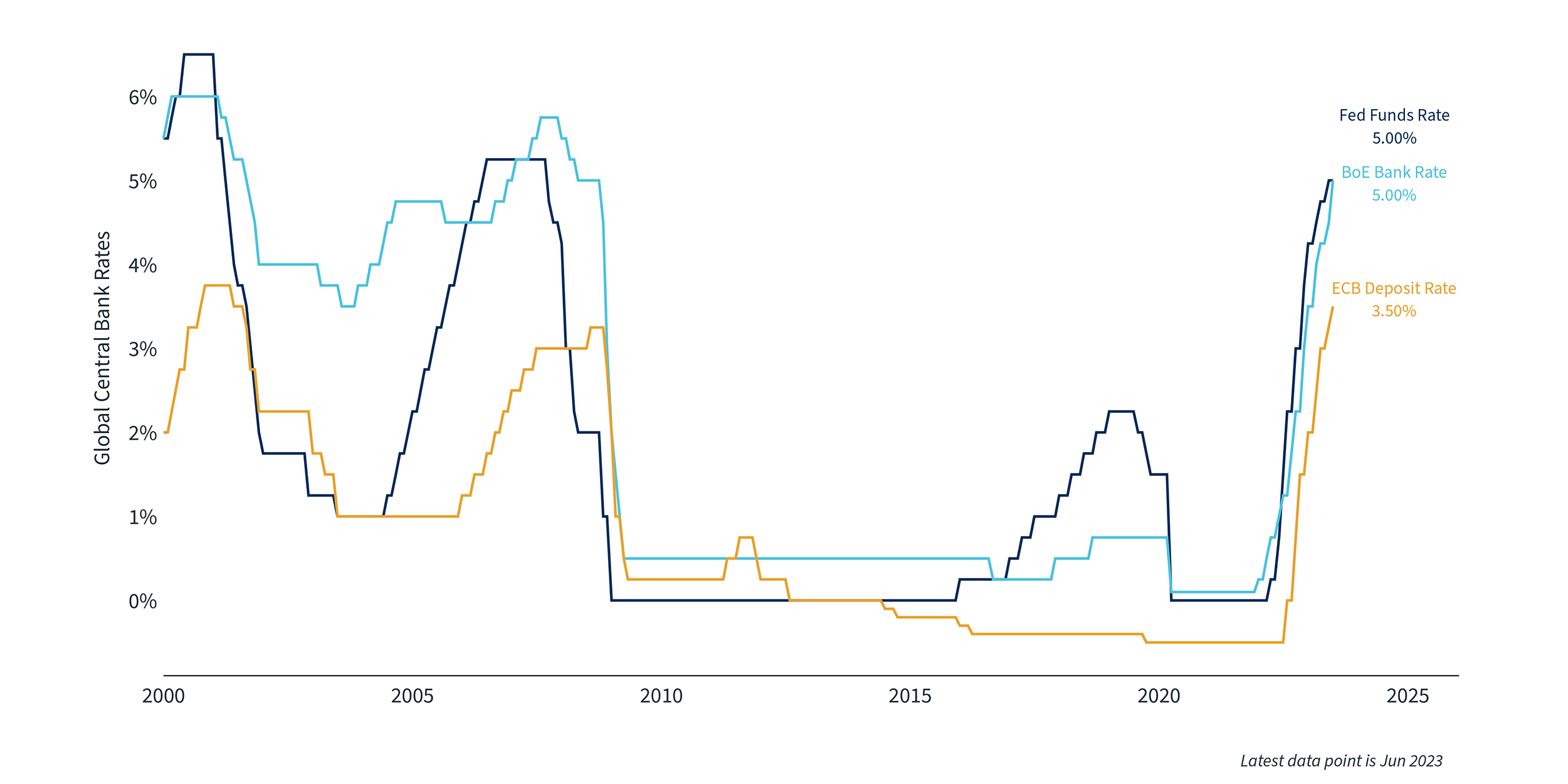

Central banks still hawkish overall but starting to go their separate ways

It can take a while for the effects of central bank increases to feed through to the real economy, and the length of the lag is unknown and can vary across time. As a result, it is too early to know if central banks have done enough to bring inflation back down to target or if they still have more to do. After 6-12 months of aggressive tightening, many central banks have slowed down on rate hikes during the first part of 2023 as inflation has come down from its highs and central bankers want time to observe the effects of prior increases. In addition to the shift in the pace of increases, after a year of almost every central bank moving in sequence, they are now moving in different directions as the declines in inflation and strength of economic growth start to vary more across economies.

In June alone, the Federal Reserve paused on their streak of hikes and left rates unchanged, while the Bank of England raised rates 50 basis points and the European Central Bank and the Bank of Canada raised rates 25 basis points. The Bank of Japan left rates unchanged, while China cut rates, just to name a few examples.

Central banks will likely continue to diverge the rest of this year as we get further away from the pandemic and local factors become more meaningful. This will have impacts on currencies, the export and import components of U.S. GDP, and the return a U.S. investor will achieve on foreign stocks and bonds.

Global Central Bank Policy Rates3

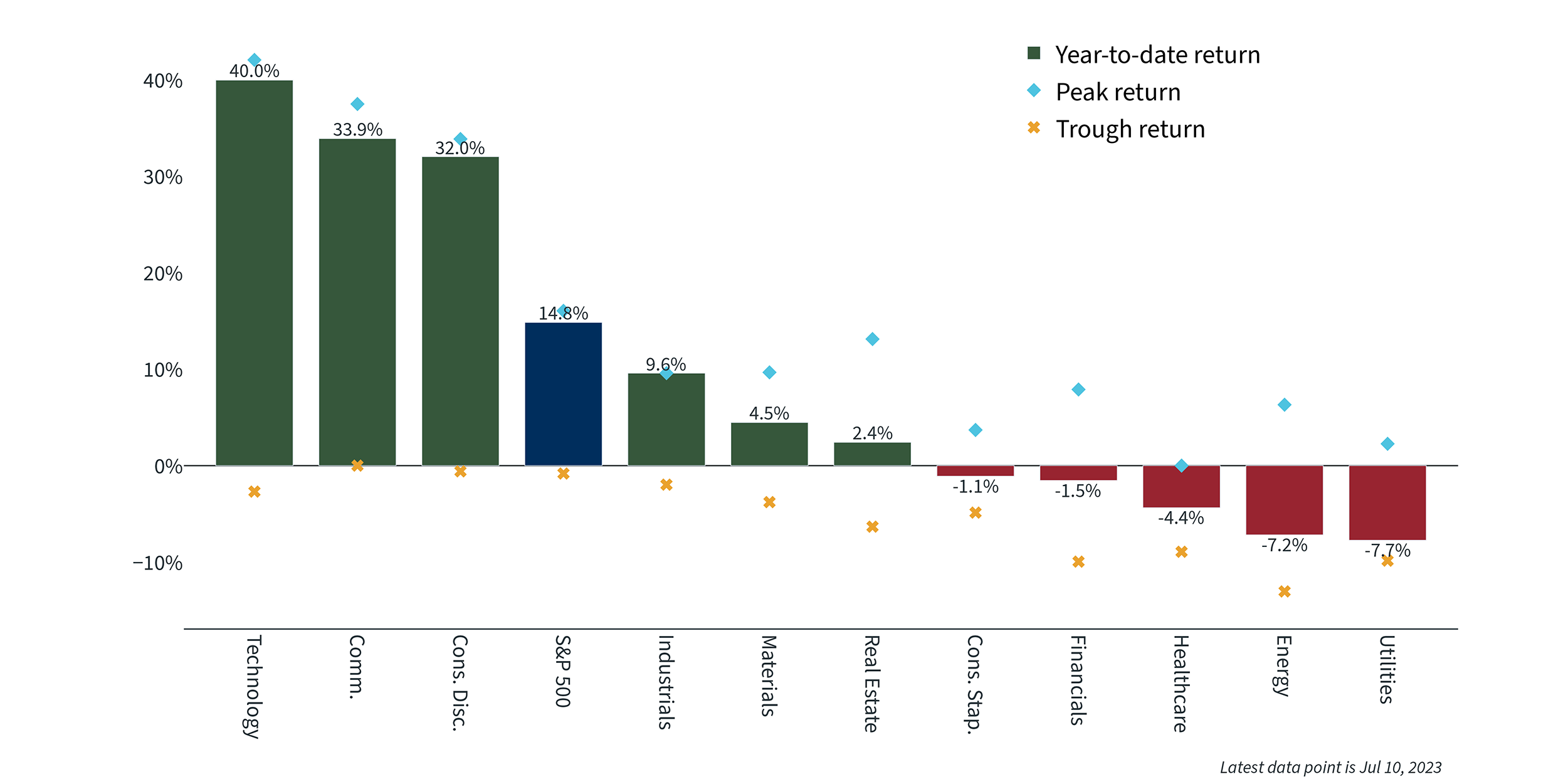

Stocks and bonds sending mixed signals

One of the more interesting factors of the current market environment is that stocks and bonds seem to be sending mixed signals about the probability of a recession. Stocks had a very strong first six months despite declining earnings and higher federal funds rates. Yet the yield curve is very inverted, especially the 2-10-year spread, which is back to almost 100 basis points. An inverted yield curve of this magnitude usually signifies a recession is imminent, though stocks have been acting like we are not just headed for a soft landing but a no-landing, where the economy keeps growing, inflation keeps falling and the Fed doesn’t have to raise rates much from here.

One explanation of the apparent disagreement between equities and fixed income is that equities are not up as much as they may appear. Large cap growth stocks are up a lot this year, particularly the so-called “Mega cap 8” (Alphabet, Amazon, Apple, Meta, Microsoft, Netflix, NVIDIA and Tesla). These stocks have driven most of the performance of equity indices this year and are the main reason the Nasdaq, up almost 30%, is dominating the Dow, which does not include these names and is up only 3%. These eight names now make up 30% of the market cap of the S&P 500, an astounding level for an index that has, as the name implies, roughly 500 constituents. The average stock in the S&P 500 is not up much and is nowhere near its price from January 2022.

The lack of breadth in the market can also be seen by comparing the S&P 500 index performance through the end of the quarter (16%) with the equal-weighted S&P 500 (6%). This represents one of the largest differences between those two indices since data started in 1990. Breadth increased during June, but it has been a fairly narrow market. This makes the difference between equity market performance and the yield curve seem like less of a contradiction, as equity performance is being driven by just a few names.

Sector Returns Year-to-Date4

Focus on long-term goals in a surprising market

The start to 2023 surprised many forecasters and economists as the economy grew more strongly than expected, stocks (or at least a few mega cap tech stocks) were up a lot and bond yields ended the quarter very close to where they started. A recession has been delayed at least a couple more quarters and inflation continues to fall. All of this has occurred despite expectations that the high point for the federal funds rate is at least 50 basis points higher than the market thought at the start of the year.

Markets can move in unusual ways, and economic data can surprise even the most knowledgeable forecaster. For the average investor, the best course of action is to maintain a well-diversified portfolio that aligns with your tolerance for risk, avoid overreacting to the latest data point and focus on your long-term goals. It was only a year ago that we saw a drastically different market, so following this steady path is a good way to avoid some of the unpredictability.

The views and opinions represented in this message are my own and do not necessarily reflect the perspective of Bremer Bank, its subsidiaries or affiliates, or its employees. This message is provided for information purposes only and nothing in it constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold any security. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor.

"CPI and Ex Food and Energy, YoY% Change." Sources: Clearnomics, Bureau of Labor Statistics

"U-3 unemployment and U-6 under-employment rates, since 1960." Sources: Clearnomics, Bureau of Labor Statistics

"Federal Reserve, Bank of England and European Central Bank Rates." Sources: Clearnomics, Federal Reserve, ECB, Bank of England

"S&P 500 sector year-to-date, peak and trough returns." Sources: Clearnomics, Standard & Poor’s, Refinitiv

About Josh Howard

Josh Howard is the Chief Investment Officer at Bremer Bank. He leads Bremer’s investment team, overseeing the development, management, delivery and communication of investment strategies and model portfolios that meet the needs of Bremer Wealth clients. Josh has more than 20 years of financial services experience, and spent seven years at the Royal Bank of Canada in a variety of investment leadership roles. Most recently, he served as Director of Global Risk Management for RBC Global Asset Management, where he managed all areas of investment risk oversight, covering equities, fixed income and alternatives as well as was responsible for deriva...

More on Josh